Adhering loans are bound by optimum loan limits set by the federal government. These limitations vary by geographic location. For 2021, the Federal Real estate Financing Agency set the baseline conforming loan limitation (CLL) at $548,250 for one-unit residential or commercial properties. Nevertheless, the FHFA sets a higher optimum loan limitation in particular parts of the nation (for instance, in New york city City or San Francisco).

The conforming mortgage limitation for a one-unit residential or commercial property in 2020. Non-conforming loans generally can't be sold or purchased by Fannie Mae and Freddie Mac, due to the loan quantity or underwriting standards. Jumbo loans are the most typical kind of non-conforming loans. They're called jumbo due to the fact that the loan amounts generally go beyond adhering loan limits.

Low-to-moderate-income purchasers purchasing a home for the first time usually rely on loans insured by the Federal Housing Administration (FHA) when they can't receive a standard loan. Customers can put down as little bit as 3. 5% of the house's purchase price. FHA loans have more-relaxed credit-score requirements than traditional loans.

There is one downside to FHA loans. All borrowers pay an in advance and yearly home mortgage insurance premium (MIP)a kind of mortgage insurance that secures the loan provider from borrower defaultfor the loan's life time. FHA loans are best for low-to-moderate earnings debtors who can't receive a standard loan average cost of timeshares item or anybody who can not manage a significant deposit.

5% deposit. The U. after my second mortgages 6 month grace period then what.S. Department of Veterans Affairs ensures home mortgages for certified service members that require no down payment. The U.S. Department of Veterans Affairs (VA) assurances house purchaser loans for certified military service members, veterans, and their partners. Borrowers can finance 100% of the loan amount with no required deposit.

The Ultimate Guide To How Many Va Mortgages Can You Have

VA loans do require a funding cost, a percentage of the loan quantity that helps offset the expense to taxpayers. The financing cost differs depending on your military service category and loan amount. The following service members do not need to pay the funding cost: Veterans getting VA benefits for a service-related disabilityVeterans who would be entitled to VA settlement for a service-related impairment if they didn't get retirement or active duty paySurviving partners of veterans who passed away in service or from a service-related special needs VA Article source loans are best for eligible active military personnel or veterans and https://www.residencestyle.com/how-can-you-explore-the-beauty-of-the-beach-and-ocean-in-real-estate/ their spouses who want extremely competitive terms and a home mortgage item customized to their monetary requirements.

Department of Agriculture (USDA) warranties loans to help make homeownership possible for low-income purchasers in rural locations nationwide. These loans need little to no money down for qualified customers, as long as residential or commercial properties meet the USDA's eligibility guidelines. USDA loans are best for homebuyers in qualified backwoods with lower family incomes, little money conserved for a down payment, and can't otherwise receive a standard loan product.

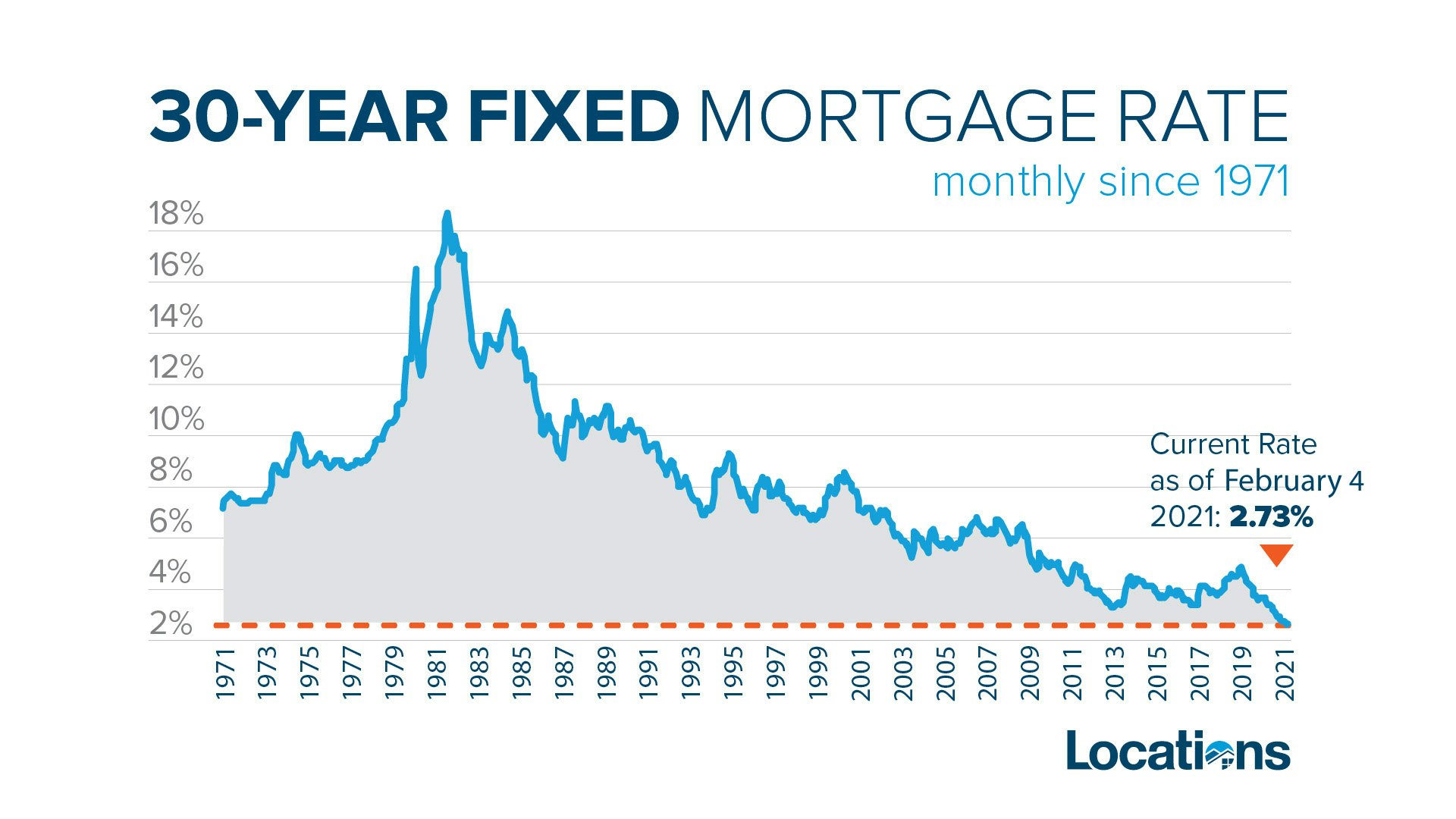

Home loan terms, consisting of the length of repayment, are a key consider how a lender costs your loan and your interest rate. Fixed-rate loans are what they seem like: A set rate of interest for the life of the loan, generally from 10 to 30 years. If you wish to pay off your house quicker and can manage a greater month-to-month payment, a shorter-term fixed-rate loan (say 15 or 20 years) assists you shave off time and interest payments.

Going with a shorter fixed-term home loan implies regular monthly payments will be greater than with a longer-term loan. Crunch the numbers to guarantee your budget plan can manage the higher payments. You might likewise wish to consider other objectives, such as saving for retirement or an emergency situation fund. Fixed-rate loans are perfect for purchasers who prepare to sit tight for several years.

However, if you have the appetite for a little threat and the resources and discipline to pay your mortgage off faster, a 15-year set loan can conserve you considerably on interest and cut your repayment duration in half. Adjustable-rate home mortgages are riskier than fixed-rate ones however can make sense if you prepare to sell your house or refinance the home loan in the near term.

Fascination About Blank Have Criminal Content When Hacking Regarding Mortgages

These loans can be risky if you're unable to pay a greater monthly home mortgage payment once the rate resets. Some ARM items have a rate cap defining that your monthly mortgage payment can not go beyond a particular amount. If so, crunch the numbers to make sure that you can possibly deal with any payment increases up to that point.

ARMs are a strong option if you don't prepare to remain in a home beyond the initial fixed-rate duration or know that you intend to refinance before the loan resets. Why? Rates of interest for ARMs tend to be lower than fixed rates in the early years of repayment, so you might possibly conserve thousands of dollars on interest payments in the initial years of homeownership.

A lot of these programs are offered based upon buyers' income or financial need. These programs, which normally provide help in the form of down payment grants, can also save novice debtors substantial cash on closing costs. The U.S. Department of Real Estate and Urban Development (HUD) lists novice property buyer programs by state.

All these loan programs (with the exception of novice homebuyer support programs) are readily available to all homebuyers, whether it's your first or 4th time buying a home. Lots of people falsely think FHA loans are available just to newbie buyers, however repeat customers can qualify as long as the buyer has not owned a primary home for at least 3 years leading up to the purchase. what are the interest rates on 30 year mortgages today.

Home mortgage loan providers can help examine your finances to assist figure out the finest loan items. They can also help you better understand the credentials requirements, which tend to be complicated. A supportive lender or home mortgage broker may likewise give you homeworktargeted locations of your finances to improveto put you in the greatest position possible to get a home mortgage and purchase a home.

Getting My How Do Balloon Fixed Rate Mortgages Work? To Work

You're entitled to one totally free credit report from each of the 3 primary reporting bureaus each year through annualcreditreport. com - when does bay county property appraiser mortgages. From there, you can find and repair mistakes, deal with paying for financial obligation, and enhance any history of late payments before you approach a mortgage loan provider. To further protect your credit report from mistakes and other suspicious marks, considering utilizing among the best credit tracking services currently readily available.

You'll have the ability to act quicker and might be taken more seriously by sellers if you have a preapproval letter in hand.

There are several types of home mortgage loans. Though many individuals merely think of a home loan as the loan utilized to purchase a home, in reality a home loan is any type of loan that is secured by home equity. Home loans can be found in several types and can be structured various methods.

A 15-year loan is typically used to a mortgage the debtor has been paying down for a variety of years. A 5-1 or 7-1 adjustable-rate home loan (ARM) may be a great choice for someone who anticipates to move again in a few years. Choosing the right type of mortgage for you depends upon the type of debtor you are and what you're wanting to do.